Wise Large Transfer Delayed Two Weeks: How Should Cross-Border Entrepreneurs Respond?

Wise large transfer delays spark fintech trust crisis; practical advice for cross-border entrepreneurs.

A Wise Business user reported 10–14 day delays on large outbound transfers, reigniting debate over whether fintech companies are becoming the traditional banks they once disrupted. This article examines the possible causes — compliance, liquidity, and risk controls — compares alternatives like Stripe Treasury, and offers actionable strategies for cross-border entrepreneurs to safeguard their cash flow.

The Trigger: Large Transfer "Held Hostage" for Two Weeks

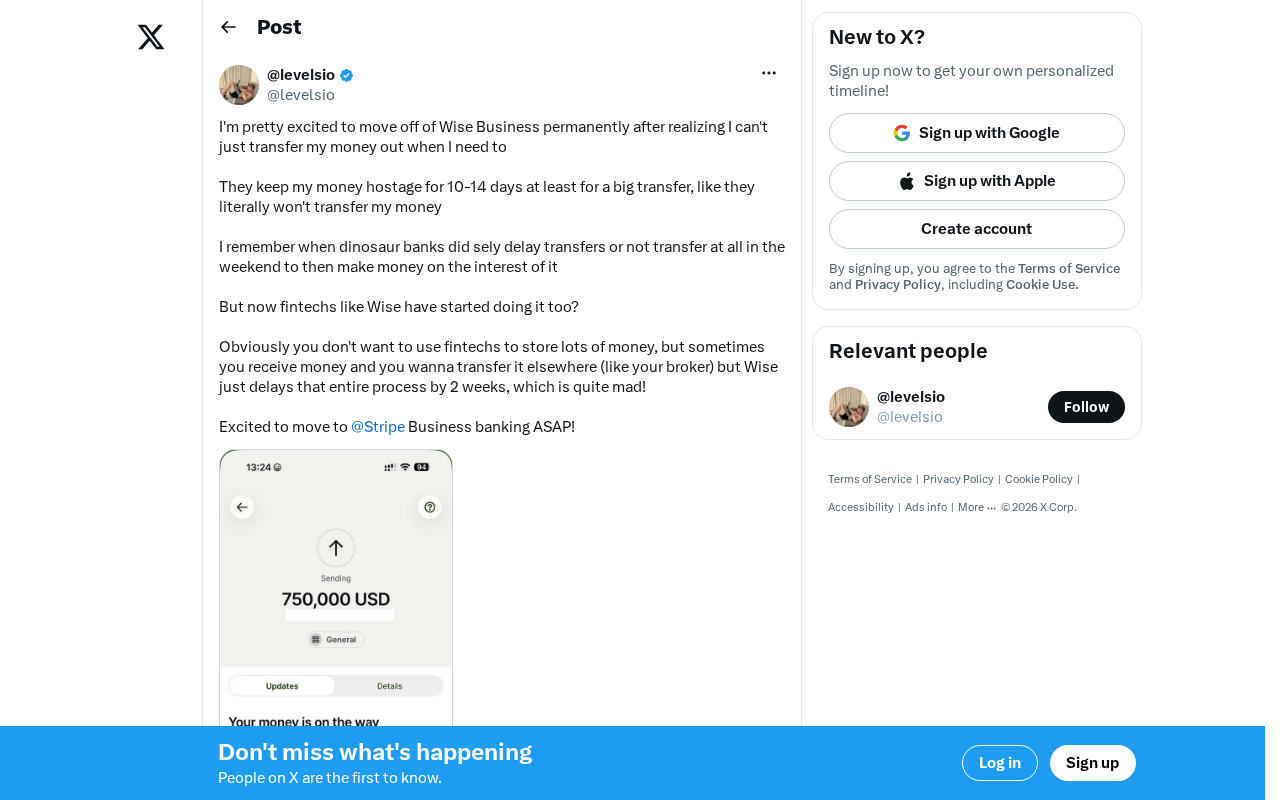

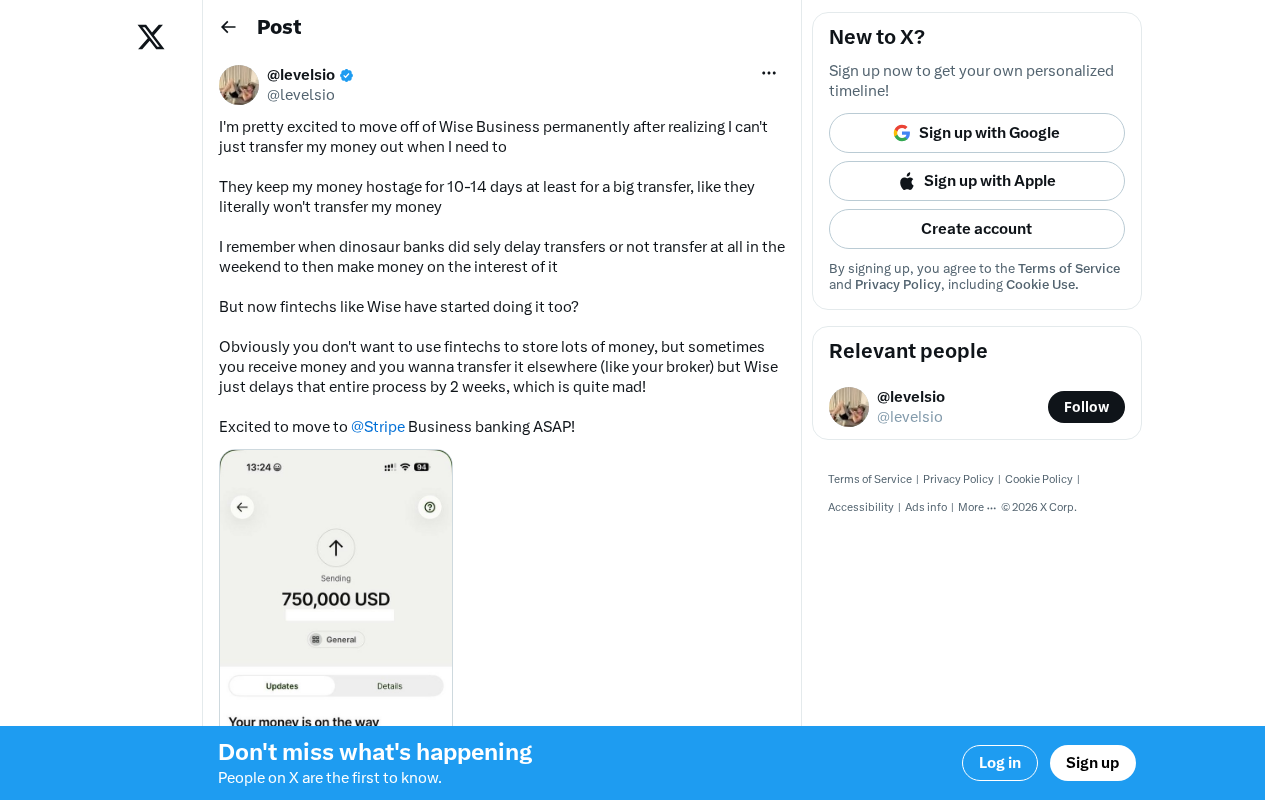

Recently, an overseas entrepreneur publicly voiced frustration with Wise Business (formerly TransferWise) on Twitter, claiming that a large outbound transfer was delayed for 10–14 days. The user bluntly stated that Wise was "holding my money hostage" and announced a permanent switch from Wise Business to Stripe's business banking services.

The tweet quickly resonated with indie developers and cross-border entrepreneurs alike — how could a fintech company known for being "fast, transparent, and low-cost" perform so much like a traditional bank when it comes to large transfers?

Is Fintech Repeating the Mistakes of Traditional Banks?

The Former Disruptor Is Now the One Being Questioned

The user made a thought-provoking comparison in the tweet:

"I remember the dinosaur-era traditional banks used to do exactly this — deliberately delay transfers, refuse to process on weekends, and profit from the interest on those funds. But now fintech companies like Wise are doing the same thing?"

This observation strikes at an uncomfortable reality in the fintech industry. Wise's original selling point was breaking through the opacity and high latency of traditional banks in cross-border transfers. Yet as the company has scaled and faced post-IPO profitability pressures, some users have begun noticing subtle shifts in the service experience.

To understand this shift, it helps to revisit Wise's business model. Wise (formerly TransferWise) was founded in 2011 by two Estonian entrepreneurs. Its core innovation was a "peer-to-peer matching" model for cross-border transfers. Unlike traditional banks that route international payments through the SWIFT network, Wise established local funding pools in various countries, effectively converting a cross-border transfer into two domestic ones. In 2021, Wise went public via a direct listing on the London Stock Exchange, with a valuation that briefly exceeded $11 billion. However, since going public, net interest income — generated from customer funds held on the platform — has become one of its significant revenue streams. This is precisely the underlying logic behind users' suspicion that Wise "deliberately delays transfers to earn interest."

Possible Reasons Behind Large Transfer Delays

To be fair, there are legitimate explanations for Wise's delays on large transfers:

-

Compliance Reviews (KYC/AML): Anti-money laundering regulations in various countries require financial institutions to conduct additional scrutiny on large transactions, which genuinely takes time. KYC (Know Your Customer) and AML (Anti-Money Laundering) are the two pillars of global financial regulation, and reporting thresholds vary dramatically across jurisdictions — the U.S. requires CTR reports for cash transactions exceeding $10,000, while the EU's Sixth Anti-Money Laundering Directive further expands the regulatory scope. For an institution like Wise operating across dozens of jurisdictions, a single large cross-border transfer may simultaneously trigger compliance reviews in both the sending and receiving countries. On top of that, the "Travel Rule" implemented by multiple countries starting in 2023 has further increased the time cost of compliance processing.

-

Liquidity Management: As a licensed electronic money institution (EMI) rather than a bank, Wise manages its funding pools differently from traditional banks. Large outbound transfers may trigger additional liquidity reviews. EMIs are required to safeguard customer funds in segregated trust accounts and cannot use them for their own operations or investments. This means that large withdrawals require coordination with custodian banks for fund allocation, objectively adding processing time.

-

Risk Control Mechanisms: Unusually large outbound transfers may automatically trigger risk control systems, leading to manual review intervention.

But the real question is — is a 10-to-14-day wait reasonable? When real-time payments have become standard in many markets, a two-week delay is genuinely hard to accept. As of 2024, over 70 countries and regions have deployed real-time payment systems: the UK's Faster Payments has enabled near-instant domestic transfers since 2008, India's UPI processes over 400 million transactions daily, and the U.S. FedNow went live in 2023. While real-time cross-border payments remain an industry challenge, the EU's upcoming "Instant Payments Regulation" will require all EU banks to support euro-area transfers within 10 seconds by 2025. Against this industry backdrop, a two-week delay is clearly out of step with user expectations.

More critically, if the delay is due to compliance requirements, did Wise adequately inform users in advance?

Real-World Impact on Cross-Border Entrepreneurs

Cash Flow Is the Lifeline

For indie developers and cross-border entrepreneurs, liquidity is everything. As the user put it: "Obviously you wouldn't want to keep large amounts of money on a fintech platform, but sometimes you receive funds and want to move them immediately — say, to a brokerage account — and Wise drags the whole process out for two weeks. That's insane."

This scenario is extremely common in real business operations: after receiving client payments, you need to quickly allocate funds to different purposes — paying suppliers, investing, or transferring to a primary bank account. Any delay at any point can trigger a chain reaction.

Can Stripe Banking Be a Viable Alternative?

The user indicated they would switch to Stripe's business banking services. Stripe has indeed been steadily expanding its financial infrastructure capabilities in recent years, evolving from a pure payment processor into a comprehensive business banking service provider.

Stripe's business banking service (Stripe Treasury) is essentially a BaaS (Banking-as-a-Service) model. Stripe Treasury doesn't operate under a bank license held directly by Stripe; instead, it partners with licensed banking partners (such as Goldman Sachs, Evolve Bank, etc.) to deliver services. This means user funds are actually held at partner banks, protected by FDIC deposit insurance (up to $250,000), while users gain programmatic fund management capabilities through Stripe's API. For developers already using Stripe for payment collection, keeping funds within the Stripe ecosystem for management can theoretically reduce cross-platform transfer friction and enable automated revenue distribution, supplier payments, and fund scheduling through code.

However, it's worth noting that any financial services platform may have similar compliance review processes for large transfers. Whether Stripe can truly deliver faster processing remains to be validated in practice. Additionally, the BaaS model carries its own risks — incidents in 2023 where multiple BaaS intermediaries faced compliance issues that led to frozen user accounts demonstrate that the more intermediary layers involved, the greater the potential for single points of failure.

Practical Advice for Developers Going Global

Based on this incident, cross-border entrepreneurs should consider the following strategies when choosing financial services:

- Don't put all your funds on a single platform: Diversify across multiple financial service providers to avoid single points of failure.

- Test large transfer processes in advance: Before you actually need to move large sums, test the platform's processing speed and workflow with a sizable amount.

- Understand the platform's license type: There are fundamental differences between electronic money institutions (EMIs), payment institutions, and banks in terms of fund protection and processing capabilities. A banking license means protection under deposit insurance schemes, while EMIs must safeguard customer funds in segregated trust accounts but don't enjoy deposit insurance and have far less flexibility in liquidity management than banks.

- Keep a traditional bank account as a backup: Despite higher fees, traditional banks often provide better guarantees for fund safety and large transaction processing.

- Set compliance timeline expectations: Before initiating a large transfer, proactively contact the platform's customer service to understand expected processing times — especially when cross-border transfers involve compliance reviews across multiple jurisdictions.

Fintech was born to make financial services faster, more transparent, and cheaper. When these platforms start behaving like the traditional institutions they once set out to disrupt, users voting with their feet is the most natural response. This also serves as a reminder to all fintech companies: building user trust takes years, but destroying it may only take one bad transfer experience.

Related articles

Building a Cold Chain Logistics Optimization Research Project with Codex: A Complete Workflow from Scratch to PDF Paper

Learn how to use OpenAI Codex to build a complete cold chain logistics optimization research project from scratch, including simulated annealing implementation, experiments, figures, and LaTeX paper compilation.

Codex Beginner's Practical Guide: Master Core AI Programming Skills in One Weekend

OpenAI Codex beginner's practical guide covering environment setup, code generation, bug fixing, and project refactoring. Includes efficient learning tips and Prompt techniques for fast AI programming mastery.

AI Agent Systematic Learning Path: From Zero to Independent Development

A systematic AI Agent learning path covering core principles, Prompt engineering, RAG, multi-Agent collaboration, and hands-on projects for beginners.